This is a deliberately simple, reproducible experiment. I used MetaTrader 5’s built-in MACD Sample Expert Advisor on a 15-minute chart, then replayed its closed trades through the PropQuant Lab simulator. The aim is not to promote the EA. It is to show why a prop-account result must be evaluated separately from a conventional backtest.

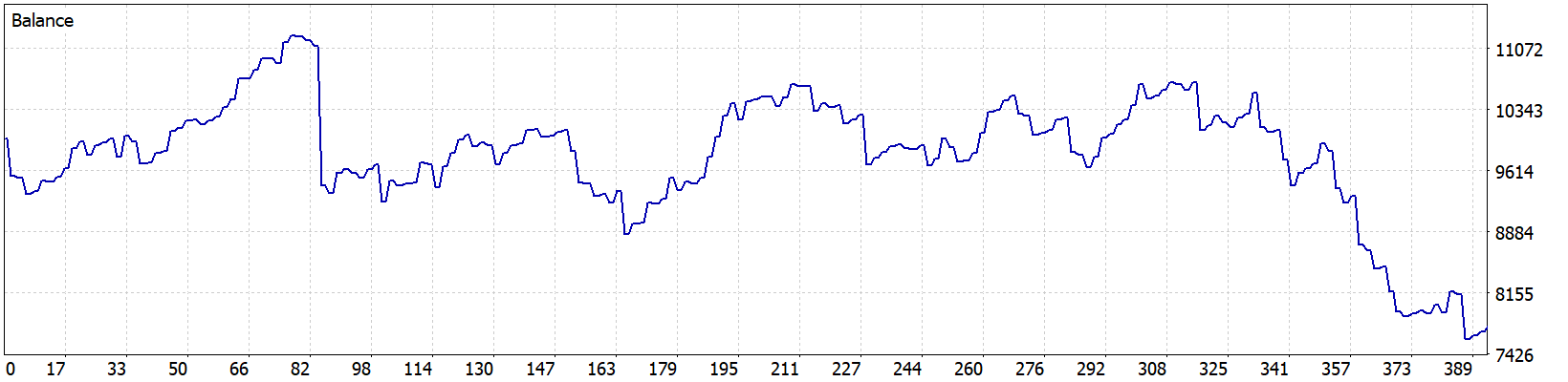

The baseline MT5 test

The conventional conclusion is correct: this configuration did not produce a positive backtest. A losing final balance is not rescued by a different account wrapper.

Why the prop-firm replay can look different

A prop challenge is path-dependent. It does not pay for the final value of the entire history. It pays when a specific sequence first reaches a target without touching a daily or overall loss limit. After a breach, the model starts another attempt and charges another challenge fee.

With the original risk setting, the $50K challenge replay was generally unattractive. The strategy often failed before reaching the target, so challenge fees accumulated faster than funded payouts. This is the situation many traders miss when they look only at the win rate or at one temporary recovery in an equity curve.

What changed at 2× risk

I then ran the exact same closed-trade history at a 2.0× risk multiplier. The trading logic did not improve. The negative final backtest did not disappear. What changed was the speed at which a winning streak could reach a challenge target.

Targets are reached too slowly. Repeated resets mean total fees can exceed withdrawals.

Net historical result: negativeWinning streaks reach targets sooner, before the later drawdown interrupts the attempt.

Net historical result: positive on selected profilesThe actual $50K 1-Step comparison

Below are the net historical payout estimates from this exact statement, using the same $50K account size and the same program settings. The only changed input is the simulator’s risk multiplier. Fees from every failed attempt are included.

Historical replay only. The 2× scenario had many more challenge attempts and breaches, so the positive totals are path-dependent rather than a smooth improvement in strategy quality.

In this historical replay, some selected prop profiles changed from fee-heavy losses to substantial positive payout estimates. That is an observation about this exact path through the sample, not evidence that the EA became profitable. A different ordering of the same wins and losses, a small spread change or one intraday drawdown can reverse the result.

The real lesson: payout optionality is not alpha

A prop program can create payout optionality: a short, favourable sequence may cross the target and produce a withdrawal before the longer-term negative drift arrives. Increasing size makes that window easier to reach. It also makes each adverse day more likely to breach the account.

| Question | What this case study says |

|---|---|

| Did the MACD Sample gain a positive expectancy? | No. The original MT5 test still ended −$2,232.70. |

| Can a negative backtest generate a historical prop payout? | Yes, if a favourable part of the path reaches a target before a breach. |

| Does 2× risk make the approach safer? | No. It increases both target speed and the chance of rapid account failure. |

| Is this a repeatable business model? | Not without evidence of a durable edge after fees, costs and many out-of-sample paths. |

When aggressive sizing is especially dangerous

Higher risk is not a generic solution for an unprofitable strategy. It is only even theoretically plausible for a distribution with frequent enough winning sequences to reach targets before its losses arrive. A near-50/50 trade distribution may provide those short clusters; a low win-rate system with rare, large wins has a very different failure profile.

- Do not infer an edge from one successful payout sequence.

- Model every retry fee, not only the first challenge purchase.

- Stress the worst daily loss, not merely the final balance drawdown.

- Use out-of-sample periods and randomised trade-order tests before relying on a streak.

- Assume real intraday equity, spread and slippage can be worse than a closed-trade replay.

Upload an MT5 HTML report, select a $50K account and compare 1.0× and 2.0× risk. Focus on attempts, breaches, fees and payouts together — not the largest green number in the table.

Open the Prop Simulator →Methodology and limitations

The replay uses closed-trade P&L from the MT5 report and the listed program profiles in PropQuant Lab. It estimates historical challenge attempts, breaches, phase passes, payout eligibility and fees. It cannot reconstruct every intraday equity movement, floating drawdown, execution delay, spread change, rule update, tax or checkout promotion. It is an educational comparison, not investment advice or a recommendation to trade an unprofitable strategy.

Primary materialsMetaTrader 5 MACD Sample source code ↗PropQuant Lab historical prop-program simulator →